Darkpool Edge

Will your dark pool survive launch?

See it in action: launch Darkpool Edge →

Japan has no shortage of dark pools. (大塚剛志, 2017; Wakamatsu, 2026)

Yet launching a viable dark pool has risks and perils. Every new PTS operator faces the same problem before launch: no empirical data, no participant history, and a fee decision that determines whether the pool reaches self-sustaining liquidity or fades away quietly at single-digit market share.

SBI Japannext and Goldman Sachs SIGMA X demonstrated that institutional order flow will migrate off-exchange, but only if the fee is right and the adverse selection risk is manageable.

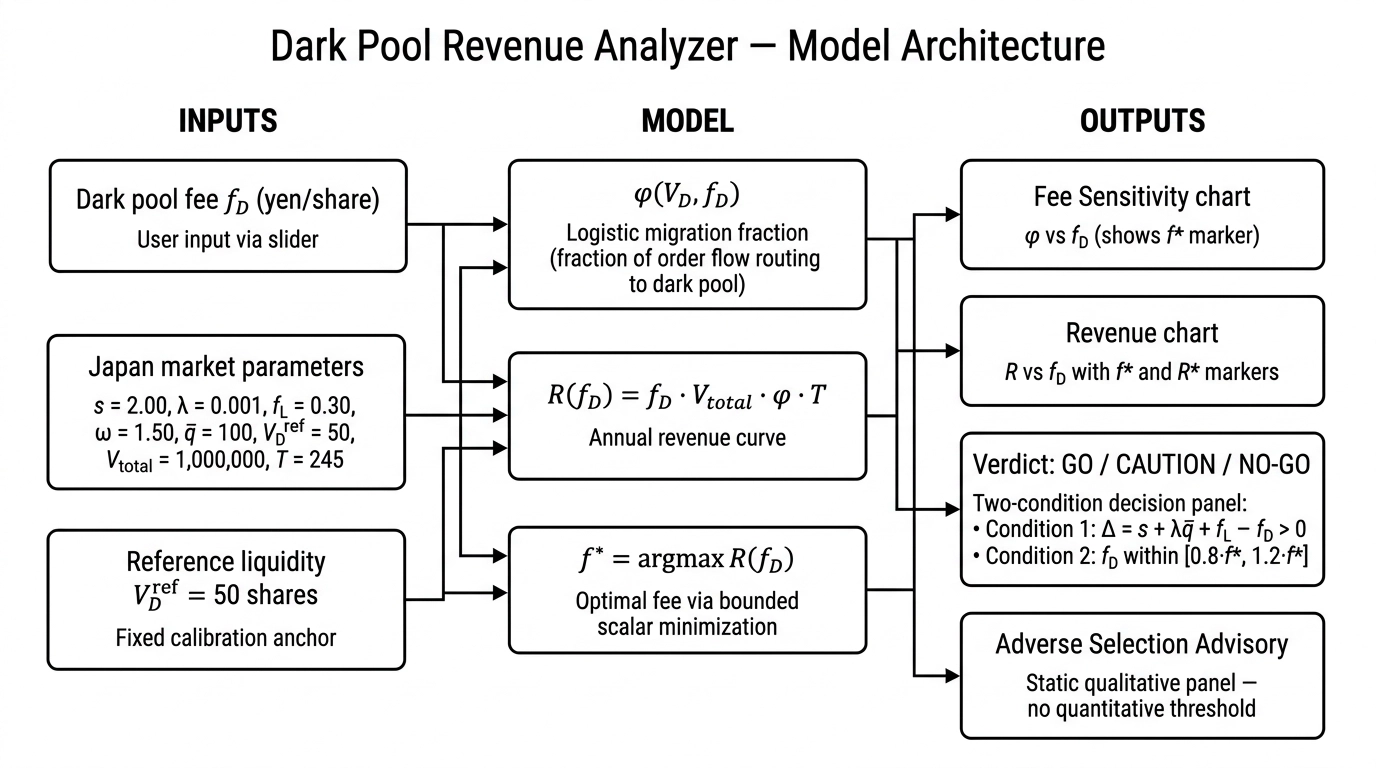

Darkpool Edge (Homayounfar, 2026) is a quantitative decision tool for PTS operators, exchange strategists, and institutional brokers designing or evaluating a dark pool in the Japanese equity market. Enter a proposed fee \(f_D\). The model returns the revenue-optimal fee \(f^*\), projected annual execution fee income \(R^*\), and a Go/No-Go verdict — all calibrated to Japan equity market parameters.

What the model returns

Revenue-optimal fee \(f^*\)

The fee that maximizes annual execution fee income, derived from the inverse elasticity condition: the point where margin gained from a fee increase exactly equals order flow lost.

Formally,

\[f^* = \arg\max_{f_D} R(f_D)\]where

\[R(f_D) = f_D \cdot V_{\text{total}} \cdot \phi(f_D) \cdot T\]This must be solved numerically as no closed form exists.

Migration fraction \(\phi\)

The share of institutional order flow that routes to the dark pool at a given fee, modeled as a logistic function of the cost advantage \(\Delta = s + \lambda\bar{q} + f_L - f_D\). Calibrated to TSE mid-cap spread and Kyle \(\lambda\) estimates from JSDA 2023–24 data.

Annual revenue projection \(R^*\)

Projected annual execution fee income per listed security at equilibrium migration over \(T = 245\) Japan trading days. Scales linearly across listings: a venue with \(N\) comparable securities implies aggregate revenue of approximately \(N \times R^*\).

Go / No-Go verdict

A two-condition decision panel.

- Condition 1: cost advantage \(\Delta > 0\) — the dark pool must be cheaper than the lit venue for the marginal trader.

- Condition 2: fee proximity to \(f^*\) — fees outside \([0.6 \cdot f^*, 1.4 \cdot f^*]\) produce a No-Go. An adverse selection advisory flags that \(\kappa_c\) cannot be computed without trade-level data and recommends a PIN-model calibration before launch.

Who it is for

- PTS operators and exchange strategists setting launch fees

- Institutional brokers evaluating venue economics before committing order flow

- Risk and compliance teams stress-testing dark pool fee scenarios

- Quant researchers modeling Japan equity market microstructure

- Pre-sales demonstrations for FSA-regulated venue design engagements

Try it

Darkpool Edge runs entirely in the browser. No installation required.

Enterprise version

The analyzer uses Japan equity market baseline parameters drawn from TSE Level 2 data, JSDA quarterly statistics, and SBI Japannext operational data. An enterprise version recalibrates the model to a client’s proprietary order flow data — participant composition records, actual execution history, and desk-specific fee scenarios — and delivers a private deployment with a three-type trader population (retail, asset manager, proprietary trading firm) and an agent-based simulation layer modeling individual routing decisions and liquidity feedback effects.

To discuss an enterprise deployment → contact us

Darkpool Edge is part of Nippofin Models — domain-specific, executable applications of Nippofin’s quantitative finance solutions, built for institutional markets.

Nippofin is the fintech business unit of Nippotica Corporation, Tokyo.