TradeScope FX

See market impact before the trade

See it in action: launch TradeScope FX →

The bigger the order, the worse the slippage

When an institutional desk places a large USD/JPY or EUR/JPY order, the act of trading moves the market against them. TradeScope FX tells you how bad — before you pull the trigger.

The Solution: TradeScope FX

TradeScope FX is a pre-trade market impact estimator for large FX orders. A desk enters a proposed order — currency pair, size, execution window, and current market conditions. The tool returns expected slippage, adverse-case slippage, and timing risk, in pips and basis points.

TradeScope FX is neither a trading system nor an executor of orders. It is a decision-support tool: trade now, slice the order, or wait for better conditions.

How TradeScope FX works

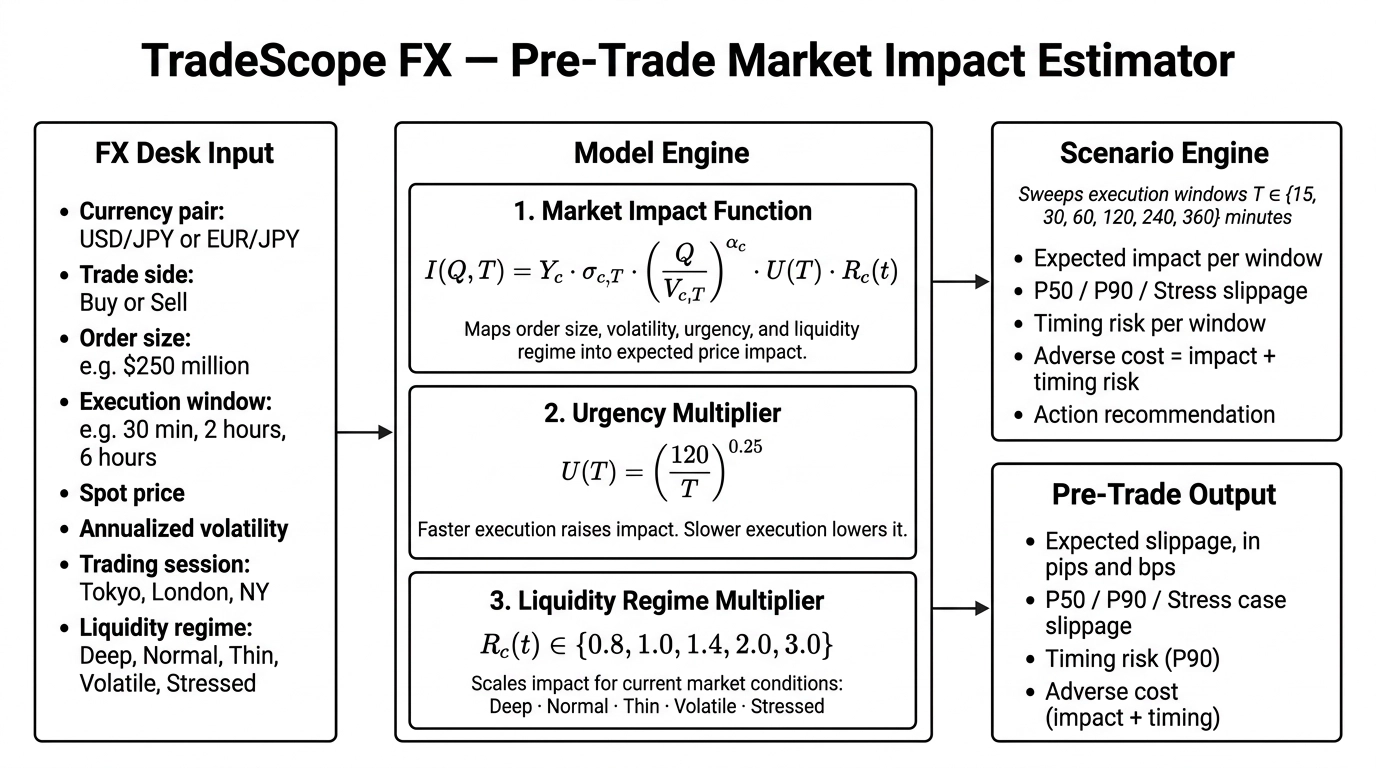

The diagram below shows the full architecture. (Evans & Lyons, 2012; Cao et al., 2026)

The FX Desk Input is where the desk enters its proposed order: currency pair, order size, execution window, spot price, volatility, trading session, and current liquidity regime. These inputs flow into the Impact Model at the centre.

The Model Engine has three components. The market impact function maps order size, volatility, and available volume into an expected price impact. An urgency multiplier adjusts that impact up or down depending on how fast the order needs to be executed — faster execution costs more. A liquidity regime multiplier scales the result for current market conditions, from deep and liquid to thin, volatile, or stressed.

Those three components feed into the Scenario Engine, which sweeps six execution windows from 15 minutes to 6 hours. For each window, it computes expected impact, adverse-case and stress scenarios, timing risk, and total adverse cost.

On the right, the Pre-Trade Output gives the desk what it needs: expected impact in pips and basis points, P90 and stress impact scenarios, timing risk at the 90th percentile, and an execution window recommendation.

The dashed arrow at the bottom shows the enterprise extension: post-trade calibration using the client’s own historical fills, realized slippage, and venue-level liquidity data. That is how the model moves from literature-based defaults to a bank-grade production estimator.

The key insight

TradeScope FX separates two costs that desks often conflate:

Market impact — the slippage caused by your own order moving the market.

Timing risk — the adverse price move that occurs while the order is still being worked.

Faster execution reduces timing risk but raises market impact. Slower execution does the opposite. TradeScope FX quantifies both sides of that trade-off, for every execution window, before the order is placed.

Currency pairs

TradeScope FX covers USD/JPY and EUR/JPY, parameterized separately.

USD/JPY is the world’s most actively traded currency pair during the Tokyo session. EUR/JPY is thinner — its effective liquidity depends on conditions in both EUR/USD and USD/JPY simultaneously. A model that treats EUR/JPY as a standalone ticker underestimates impact during periods of stress in either leg. TradeScope FX accounts for this.

Who it is for

- Asset managers with overseas bond portfolios

- Life insurers executing currency hedges

- Trust banks managing large repatriation flows

- Corporate treasury desks settling cross-border transactions

- FX brokers serving institutional clients

- Securities firms and regional banks with USD/JPY or EUR/JPY execution desks

Try it

TradeScope FX is available as an interactive web application.

Enterprise version

The current version uses literature-based parameters. The enterprise version is calibrated to the client’s own execution history — historical parent orders, child orders, fills, benchmark prices, and realized slippage. It also includes venue-level liquidity modeling and an audit trail for best-execution governance.

To discuss a calibration PoC → contact us

TradeScope FX is part of Nippofin Models — domain-specific, executable applications of Nippofin’s quantitative finance solutions, built for institutional market.

Nippofin is the fintech business unit of Nippotica Corporation, Tokyo.