FlowState monitors directional information flow between global equity markets, updated daily.

You specify the market pairs; FlowState tells you which is currently leading which — and how persistently — using Transfer Entropy (Schreiber, 2000) rather than correlation. The output is a ranked signal feed your desk can act on.

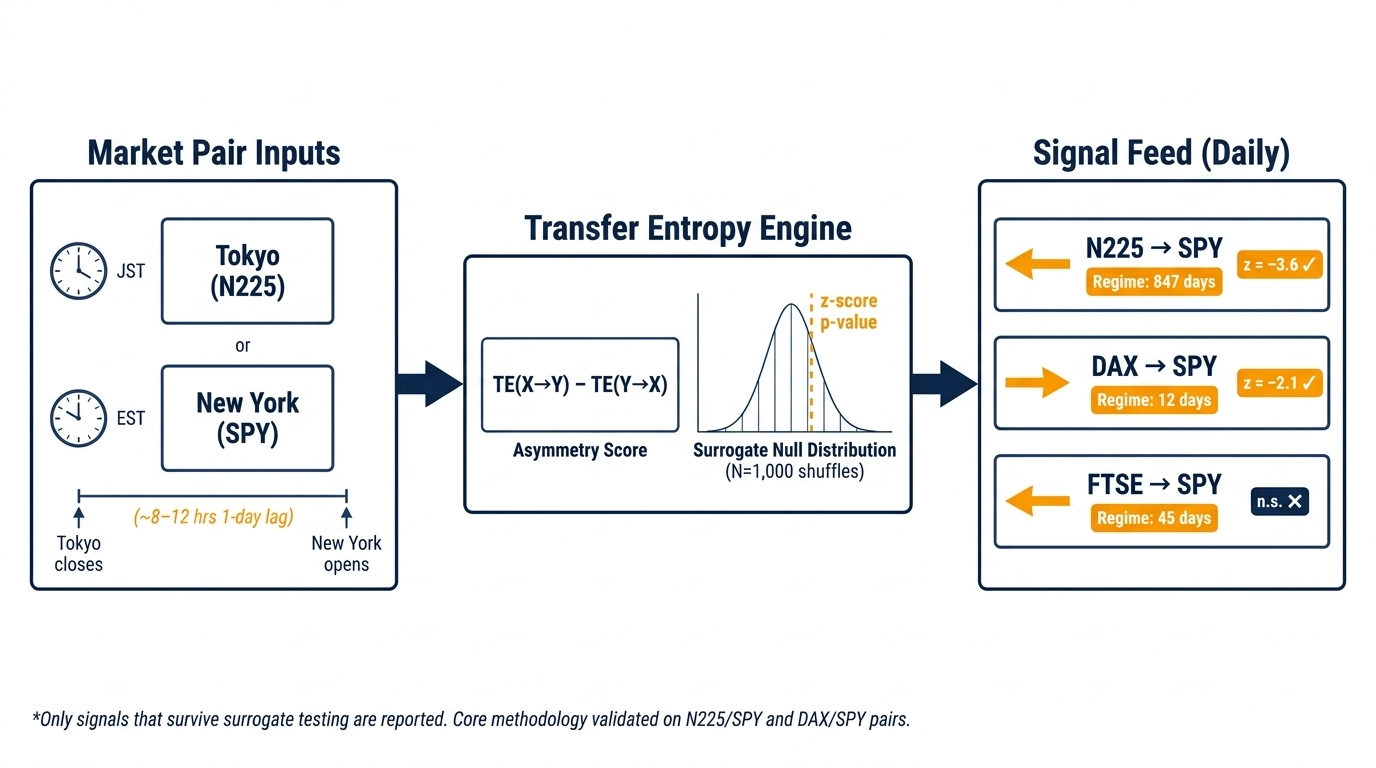

FlowState has a three-stage pipeline: market pair inputs (Tokyo/New York) with their ~8–12 hour lag annotated, a central Transfer Entropy Engine that computes a directional asymmetry score and validates it against 1,000 surrogate shuffles, and a ranked daily signal feed on the right showing which market leads which, how long the regime has persisted, and whether the signal is statistically significant.

What Makes It Unique

Direction, not just co-movement. Correlation tells you markets are linked. FlowState tells you which one moves first — a distinction that can remain hidden for years in standard tools.

Regime persistence scoring. Every signal is tagged with how long the directional relationship has been active, so you can distinguish a durable structural regime from a one-week artifact.

Statistically validated. Each asymmetry reading is benchmarked against a surrogate null distribution, giving you a z-score and p-value alongside the signal — not just a number.

Use Cases

Detect carry-trade regime shifts before they show up in volatility — position ahead of the unwind, not after.

Validate whether an overnight move in your book is noise or the continuation of a persistent directional flow.

Benchmark your cross-market assumptions quarterly: is the leader-follower relationship you modeled six months ago still the one in the data?

Methodology

Every day, FlowState asks: does knowing what Tokyo did yesterday actually help predict what New York does today — more than New York’s own history does? If yes, and by how much, and in which direction?

That question is answered using Transfer Entropy, a technique from information theory that measures directional influence without assuming markets behave in any particular way. (Dimpfl & Peter, 2018; Kuang, 2021)

To make sure the signal is real and not a statistical fluke, each result is stress-tested against 1,000 randomly shuffled versions of the same data. Only signals that survive that test are reported.

Core methodology validated on N225/SPY and DAX/SPY pairs. Additional exchange pairs — including HSI, FTSE, ASX, and others — available on request, subject to validation.

Information flow among stock markets leads to the co-movement of stock prices and even the financial risk contagion globally. Measuring information flow on multi time-scales helps to develop optimal portfolio strategy for market participants and establish targeted financial regulation for policy makers, but is a challenge for traditional econometrics. This study aims to construct the information flow networks on multi time-scales among international stock markets. First, we use the data of 31 stock market indices during 2007 to 2018, and decompose each of stock index series into short and mid-long time-scale components by empirical mode decomposition (EMD). Then, we extend a novel concept in information science, called transfer entropy (TE), to measure information flow and characterize causality structure between two stock markets, and find that information flows inside of EU stock markets only cluster on short time-scale but not on mid-long time-scale. Moreover, both out-node and in-node centrality measurements for developed markets in the entropy-based networks are much higher on short time-scale, indicating that these markets are more dominant but more vulnerable to short-term risk contagion. Finally, based on the minimum spanning tree (MST) model, we extract the most probable risk contagion paths from entropy-based networks. The results show that outflow MSTs on short time-scale follow a star-like structure to precipitate the risk contagion in the international stock markets, especially during crisis period (2007∼ 2010). Overall, we emphasize the financial risk contagion on short time-scale.

2018

Elsevier

Analyzing volatility transmission using group transfer entropy

We analyze the transmission of volatility between the oil, stock, gold, and currency markets using transfer entropy. Our approach, which we denote by group transfer entropy, measures the overall sensitivity of a process to lagged realizations of a group of other processes. We supplement our measure by a suitable block bootstrap approach which allows to conduct inference. Our empirical analysis uses daily data of OVX, VIX, GVZ, and EVZ from 2008 to 2017. The results show that oil and stock market volatility are the most affected by past volatility changes in the other markets, which highlights the importance for investors to hedge against this predictable risk transmission. Furthermore, we show that group transfer entropy can unveil nonlinear dynamics beyond the standard vector autoregressive methodology and provides a useful basis for forecast averaging.

An information theoretic measure is derived that quantifies the statistical coherence between systems evolving in time. The standard time delayed mutual information fails to distinguish information that is actually exchanged from shared information due to common history and input signals. In our new approach, these influences are excluded by appropriate conditioning of transition probabilities. The resulting transfer entropy is able to distinguish effectively driving and responding elements and to detect asymmetry in the interaction of subsystems.